When the Floor Looks Like Protection

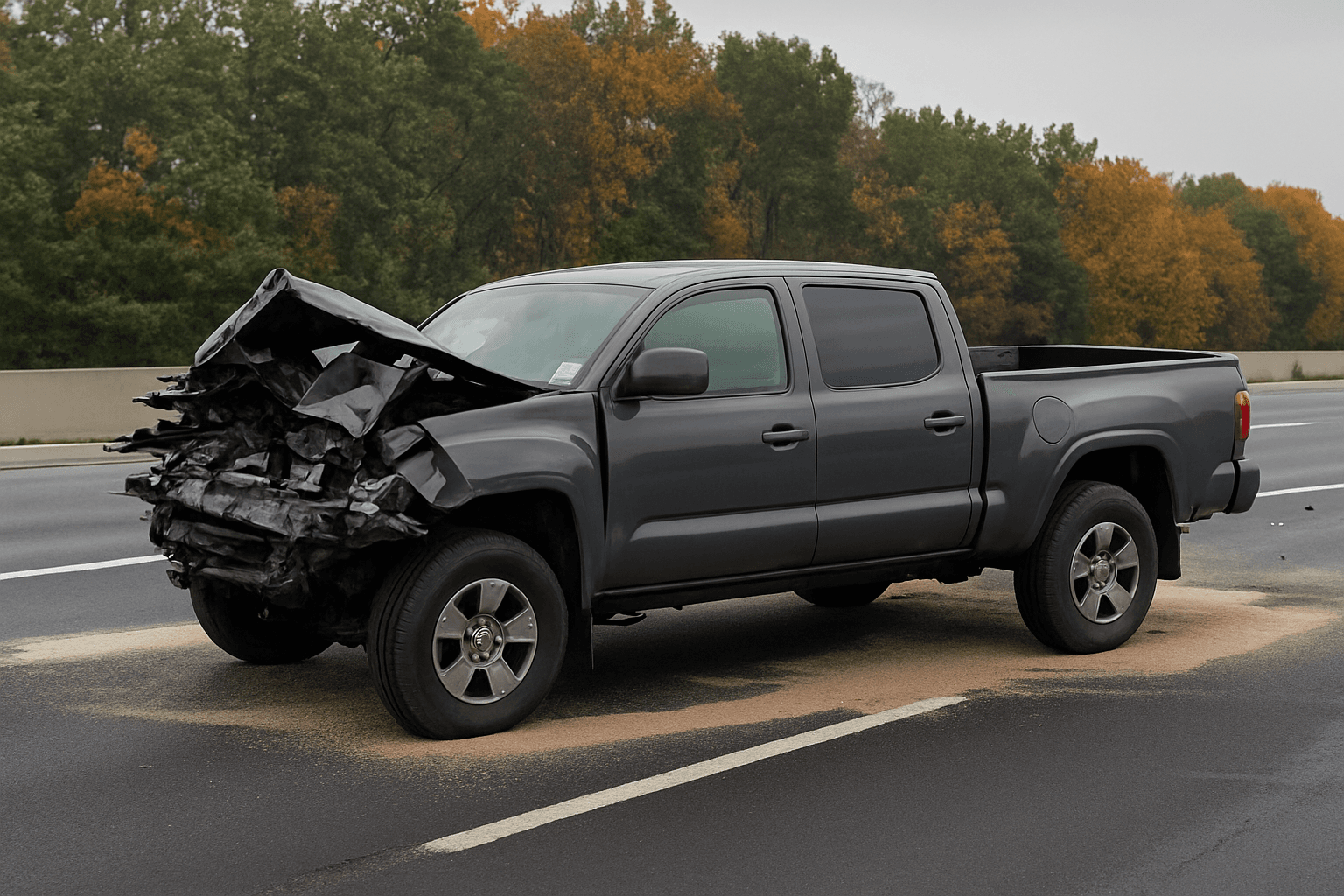

You carry Georgia's minimum liability limits because the law requires it and the paid-off car does not justify comprehensive or collision premiums. The policy satisfies the registration requirement and the DMV's GEICS compliance check passes every month. Then someone runs a red light into your lane and you are at fault for the swerve that causes the crash.

The question is not whether minimum coverage is legal. It is. The question is whether the state's floor protects you from lawsuit exposure when the crash involves multiple injured parties or a single serious injury whose medical costs exceed the per-person cap. Most budget drivers assume legal compliance equals financial protection. Georgia's liability structure demonstrates why that assumption fails.

Find the minimum coverage that meets your state's requirements

Compare liability-only rates from carriers in your state — and see what discounts you qualify for.

Get Your Free QuoteGeorgia Per-Person Bodily Injury Floor

$25,000

Georgia requires $25,000 bodily injury coverage per person, $50,000 per accident, and $25,000 property damage. A single injured party whose hospital stay and follow-up treatment exceed the per-person limit pursues the gap directly against your assets and wages.

Georgia Department of Insurance, O.C.G.A. Title 33

What the Minimum Actually Covers

Georgia's $25,000/$50,000/$25,000 minimum liability structure covers three distinct buckets. The first $25,000 pays bodily injury costs for any single injured person in the other vehicle. The $50,000 per-accident cap applies when multiple people are injured: the insurer pays up to $25,000 per person but no more than $50,000 total across all injured parties in that one crash. The $25,000 property damage limit covers the other driver's vehicle, fence, guardrail, or storefront you hit.

These limits operate as hard caps. When an injured driver's emergency room visit, surgery, physical therapy, and lost wages add to more than $25,000, your insurer pays the $25,000 limit and stops. The injured party then files a claim against you personally for the remainder. Georgia is a tort state: the at-fault driver holds full liability for damages caused, and the minimum coverage you carry does not erase that liability. It simply shifts the first $25,000 of exposure to the insurer.

The property damage floor creates the same structure. Replacing a totaled late-model SUV costs more than $25,000. Your policy pays the limit; you hold personal liability for the difference between the limit and the actual replacement cost. The lienholder on the other driver's financed vehicle does not care what your policy covers. They pursue the gap.

Georgia's minimum satisfies the law, not the lawsuit. You remain personally liable for every dollar of bodily injury or property damage beyond the caps your policy actually pays.

The Crash Georgia's Minimum Cannot Cover

You are at fault for a two-car crash. The other vehicle carries a driver and a passenger. The driver sustains a fractured pelvis requiring surgery, a three-day hospital stay, and eight weeks of physical therapy. The passenger sustains a concussion and soft-tissue injuries requiring an ER visit and follow-up neurology appointments. Your $25,000 per-person limit pays the driver's costs up to the cap, then stops. The driver's total medical costs and lost wages exceed the limit. Your $50,000 per-accident cap pays the passenger's costs, but the driver already consumed $25,000 of that total cap, leaving $25,000 available for the passenger. The passenger's bills exceed what remains under the cap.

Both injured parties now hold claims against you personally for the amounts exceeding what your insurer paid. The other driver's vehicle is totaled. Replacement cost exceeds your $25,000 property damage limit. The lienholder pursues you for the gap between your limit and the payoff balance. Georgia law permits wage garnishment and asset liens to satisfy these judgments. Minimum liability bought you legal compliance. It did not buy you protection from the financial consequences of a crash whose costs exceed the caps.

Where Budget Drivers Hold Uninsured Risk

The structural gap sits between what the law requires and what a lawsuit can reach. Georgia's GEICS system enforces continuous coverage at the minimum level, and uninsured motorist violations trigger license and registration suspensions. The enforcement mechanism ensures you carry the floor. It does not ensure the floor is sufficient to cover the damages you cause.

Most budget drivers on minimum coverage own older paid-off vehicles and have made the rational decision to drop collision and comprehensive. Liability-only makes sense when the vehicle's value does not justify the premium cost of physical-damage coverage. But that same vehicle-value calculation does not change the bodily injury or property damage exposure you create when you cause a crash. The decision to self-insure the car is separate from the decision to carry only minimum liability for damages to others.

Uninsured motorist coverage adds a backstop when the other driver hits you and carries no insurance or insufficient limits. Georgia does not mandate UM coverage, and dropping it trims the premium. The trade-off: when an uninsured driver totals your older car, you hold the full loss. UM property damage would have covered the gap between the other driver's ability to pay and your vehicle's actual cash value. Without it, you absorb that gap.

The lapse risk amplifies on a tight budget. Georgia's GEICS system reports policy cancellations to the Department of Revenue in near-real time. A nonpayment lapse triggers a registration suspension notice. The reinstatement process requires proof of continuous coverage, a $200 registration reinstatement fee, and often SR-22 filing for three years post-reinstatement. The cheapest policy that lapses becomes the most expensive decision a budget driver makes, because the reinstatement fee stack and SR-22 premium surcharge erase years of the savings the minimum policy generated.

Georgia Registration Reinstatement Fee

$200

Georgia charges a $200 registration reinstatement fee for lapse-related suspensions, separate from any license reinstatement fees. The lapse that saved one month's premium costs $200 to unwind, plus SR-22 filing requirements that elevate premiums for three years.

Georgia Department of Revenue

When Higher Limits Make Sense

Raising bodily injury limits to $50,000/$100,000 or $100,000/$300,000 costs more monthly but narrows the lawsuit exposure gap. The honest cost-benefit question: what do you own that a judgment creditor can reach, and what are you willing to risk losing to preserve the monthly savings minimum coverage offers? Georgia permits wage garnishment up to 25% of disposable earnings to satisfy judgments. If you own a home with equity, hold retirement accounts outside bankruptcy protection, or earn wages a creditor can garnish, higher liability limits shift more of that exposure back to the insurer.

The counter-case: if you own minimal attachable assets, rent rather than own, and earn limited wages, the financial advantage of pursuing you personally diminishes for the injured party. Higher limits still provide protection, but the urgency calculation changes when the judgment-proof position is real rather than assumed. This is not legal advice. It is the structural reality many fixed-income budget drivers navigate when they choose minimum coverage knowingly rather than by default.

The Comparison Step That Pays

Georgia's non-standard and high-risk specialist carrier tier writes minimum-coverage policies for drivers standard carriers decline or price out of reach. Acceptance, Bristol West, Dairyland, Direct Auto, GAINSCO, and The General all write in Georgia and offer online or phone quotes. Rate spreads between carriers writing the same driver profile often exceed the cost difference between minimum and mid-tier liability limits at a single carrier. A non-standard carrier quoting $85 monthly for minimum coverage may be undercut by a competitor at $70 for the same limits, and that $15 monthly difference funds a meaningful limit increase at the cheaper carrier.

The multi-quote discipline matters more at the minimum coverage level than anywhere else in the auto insurance market, because every dollar of premium saved is a dollar the budget driver kept rather than a percentage trim on a large bill. Comparing five carriers takes two hours. The savings persist for the full policy term, and the re-shop opportunity recurs every six or twelve months when the renewal arrives.

What to Do Right Now

Pull your current Georgia auto policy declarations page and confirm the liability limits shown. If the limits are $25,000/$50,000/$25,000, you carry the state minimum. Request quotes for $50,000/$100,000/$50,000 and $100,000/$300,000/$100,000 from three non-standard carriers writing in Georgia. Compare the monthly premium difference between your current minimum-limit policy and the mid-tier limit quote at the cheapest competitor. Run the annual cost difference against what you own that a lawsuit judgment can attach. If the gap is narrow and you hold attachable assets or wages, the mid-tier limit buys meaningful protection. If the gap is wide and your judgment-proof position is real, minimum coverage may still be the rational floor. The decision is yours, but make it with the structural trade-off visible.